As American workers approach their retirement age, they often wonder what to expect in terms of monthly Social Security benefits. Your benefit amount is directly impacted by your lifetime earnings, upon which Social Security taxes were collected to support benefit payments during retirement.

To get an estimate of your monthly benefit, you can visit https://www.ssa.gov/benefits/retirement/estimator.html to use the Social Security Administration’s Retirement Estimator tool. The methodology for calculating a monthly Social Security benefit amount can be difficult to understand, so we’ll explore the formula here.

Qualifying for Social Security

To collect Social Security benefits, you’ll need to meet the following requirements:

> 10 years (40 quarters) of “gainful” employment – in 2018, at least $1,320 of earnings are required for a fiscal quarter to count as a credit towards the total of 40 quarters

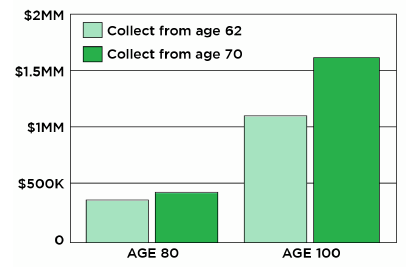

> Aged 62 years or older (if you begin drawing on Social Security at age 62, you will collect a smaller benefit amount than if you started drawing on it at age 66 and 4 months, as the benefits would be spread over a longer time period – see the chart here)

How are Social Security benefits calculated?

Americans earn Social Security benefits by paying Social Security taxes. Those taxes amount to 6.2% of your income with an upper limit on the total amount taxed – that limit is $128,400 in 2018. Additionally, employers match your payment, meaning that a total amount equal to 12.4% of your earnings are contributed to Social Security.

The more you earn over your lifetime, the higher your monthly benefit payment during retirement – the Social Security Administration has calculated the amount you’ve contributed during your years of work and associated this amount with your Social Security Number, so when you go to draw on this amount, they can easily calculate your benefit.

But how is that benefit calculated? The challenge the SSA deals with is that inflation changes the value of the dollar relative to the wage paid at the time the work was done to what that wage would earn today – whether you’re a plumber, waiter, banker, truck driver, or engineer, your wage is almost certainly much higher in 2018 than it would have been in 1978. That’s not because those jobs have become more lucrative, but because wages increase across the board in step with normal economic inflation and a general increase in the standard of living over that period.

To account for this, the SSA calculates what’s called your average indexed monthly earnings (AIME) to account for changes in average wages since your Social Security taxes were collected. The AIME is based on the 35 years in which you earned the most.

How can I estimate my Social Security Benefits?

To calculate your AIME, and in turn, your monthly Social Security retirement benefit (called “primary insurance amount” or PIA), the SSA provides a spreadsheet with instructions that will allow you to get an estimate. However, when you start drawing your benefits, the SSA will do this calculation for you to determine the amount you receive.

We recommend using their spreadsheet to get your estimate, but here’s a summary of how it works as of 2018:

- First, you’ll compile all your income by year, and multiply them by the SSA’s index factors for calculating the indexed earnings.

- Using the indexed earnings numbers, you’ll choose the 35 years that you earned the most and add them up.

- Divide the result by 420, which is the number of months in 35 years. This gives you your AIME –an average of your monthly earnings over your lifetime, adjusted for inflation and standard of living increases.

- Multiply the first $895 of your AIME by 90%, the amount over $895 and less than or equal to $5397 by 32%, and the remainder by 15%. Add this up and round the sum down to the nearest dollar to calculate your PIA.

- Your PIA is figured based on a retirement age of 66 years and 4 months.

Are there any other factors that can affect my Social Security benefit amount?

Your benefit amount may be different based on the following:

> If you choose to retire and start collecting benefits early, your monthly benefit amount will be less based on spreading the payments over a longer retirement period.

> You can also delay retirement and collection of benefits until after your full retirement age (66 years and 4 months) until you reach age 70, increasing your benefit amount accordingly.

> If you are still working but decide to collect Social Security benefits, your benefit amount will be different.

> If you are a government worker with a pension, a different formula is used for your benefits.

> Cost-of-living increases may be added to your benefit beginning with the year you reach 62, which will affect your future benefit amount.

> Benefit amounts may be lower in the future because, according to the SSA, “by 2034, the payroll taxes collected will be enough to pay only about 77 cents for each dollar of scheduled benefits.”

> If you are receiving benefits as a spouse, child, or survivor, a different calculation applies.

I’m not yet close to retirement age – what should I be thinking about at this stage?

Considering that your income will directly impact your Social Security retirement benefits, the earlier you start thinking about your retirement, the better. You should choose an occupation that will support you and your family’s lifestyle both before and after retirement.

Your income will be taxed up to $128,400 for Social Security purposes – so this is the “upper limit” of personal income that makes a difference for Social Security benefits. Additionally, consider the thresholds at which your AIME will figure differently into your PIA:

> Up to $895 – 90%

> $895 to $5,397 – 32%

> Over $5,397 – 15%

Let’s look at where these thresholds fall in terms of annual income – remember, $128,400 is the max for Social Security purposes.

> $895 x 12 months = $10,740

> $5,397 x 12 months = $64,764

Using 2018’s numbers as a baseline, everyone making $10,740 a year or less will receive 90% of that amount in their monthly Social Security benefits based on their PIA. However, the next $54,024 only earns a benefit of 32%, and the next $62,326 after that earns a benefit of 15% in Social Security retirement.

This creates a stair-step effect of benefit amounts based on your income level during your earning years. How would this play out based on some average yearly incomes for common occupations? Note that the chart below assumes 35 years of work at this mean income level supplied by the BLS for the occupation in May 2017 (the latest report available).

| Occupational Area | Average Yearly Income | Estimated Yearly SS Benefits |

| Management | $119,910 | $35,225 |

| Legal | $107,370 | $33,344 |

| Computer and Mathematical | $89,810 | $30,710 |

| Architecture and Engineering | $86,190 | $30,167 |

| Business and Finance | $76,330 | $28,688 |

| Education, Training and Library | $55,470 | $23,979 |

| Construction and Extraction | $49,930 | $22,206 |

| Building and Grounds Cleaning and Maintenance | $28,930 | $15,486 |

| Farming, Fishing and Forestry | $28,840 | $15,458 |

| Personal Care and Service | $27,270 | $14,955 |

| Food Preparation and Serving Related | $24,710 | $14,136 |

Your choice of career will certainly affect your Social Security retirement. The earlier you can think about your career path, the better.

Citations

https://www.ssa.gov/pubs/EN-05-10070.pdf

https://www.ssa.gov/benefits/retirement/estimator.html

https://www.ssa.gov/planners/retire/1943.html

https://www.bls.gov/oes/current/oes_nat.htm

Click here to read more.