Most people tend to underestimate their life expectancy. But thinking you might live to a very old age might lead to better planning decisions.

Life expectancy is a critical element in Social Security planning. Because benefits continue for life, the total amount you stand to receive over your lifetime hinges on how long you and your spouse live. In fact, we could add a new strategy for maximizing Social Security benefits — to live a really, really long time. Nothing maximizes total Social Security benefits more than extreme longevity.

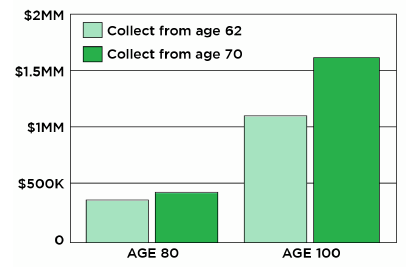

If a 62-year-old person with a primary insurance amount (PIA) of $2,000 starts Social Security now, he will receive a total of $411,130 if he lives to age 80, versus $1,048,270 if he lives to 100, assuming 2% annual cost-of-living adjustments. He can more than double his take by living an extra 20 years. If he waits until age 70 to start Social Security, he’ll receive $451,680 by age 80, or $1,573,047 by age 100, or nearly three times the earlier-death amount. This is in contrast to other retirement resources which diminish as the years go by.

Life expectancy has increased dramatically in recent years, but people’s thinking hasn’t kept up with it. Most people think they will live to be around 80, according to the Society of Actuaries. This thinking probably comes from a combination of what people understand about average life expectancies and how long their grandparents lived.

But there is some evidence that you – yes, you — could be among those who will end up maximizing Social Security benefits through extreme longevity. A new book titled The Longevity Project: Surprising Discoveries for Health and Long Life from the Landmark Eight-Decade Study has discovered that the key to a healthy, long life is not doing specific things such as exercising or eating vegetables, but rather living a conscientious life. This means being prudent, persistent, and well organized – the same traits that would lead a person to plan for retirement and seek the services of a financial advisor.

In other words, if you are asking about when you should file for Social Security and how you can maximize your benefits, you are likely to be one of the ones who will maximize those benefits by living a long life. And you will continue to do so by simply continuing to live. I once heard an interviewer ask a very old woman how she managed to live such a long life. Her response: “You can’t help it. You just keep waking up in the morning.”

So I would urge you not to buy into the statistical averages when choosing a life expectancy for retirement planning purposes. Rather, envision yourself in extreme old age. What if you just keep waking up in the morning? What if you get to be 90, 95, 100, 105?

I’ll bet if you were to ask any person who has attained one of these advanced ages if he or she thought they would ever get here, they would say no. As Eubie Blake famously said at age 100: “If I’d known I was gonna live this long, I’d have taken better care of myself.” If I may paraphrase, many people contemplating the Social Security decision may end up saying, “If I’d known I was gonna live this long, I’d have waited until I was 70 to apply for Social Security.”

As you know, delaying the onset of benefits is the very best way to maximize Social Security in the event of extreme longevity. It means forgoing a few years of benefits in your 60s, but you’ll make it up on the other end. So when planning your retirement, consider the value of Social Security over a very long lifetime, just in case you — or your spouse — makes it that long.

By Elaine Floyd, CFP®

As director of retirement and life planning for Horsesmouth, Elaine Floyd helps advisors better serve their clients by understanding the practical and technical aspects of retirement income planning. A former wirehouse broker, she earned her CFP designation in 1986.

*Carol Gosho, Principal, Gosho Financial Group with Securities offered through TD Ameritrade Institutional, Member FINRA/SIPC.

IMPORTANT NOTICE This reprint is provided exclusively for use by the licensee, including for client education, and is subject to applicable copyright laws. Unauthorized use, reproduction or distribution of this material is a violation of federal law and punishable by civil and criminal penalty. This material is furnished “as is” without warranty of any kind. Its accuracy and completeness is not guaranteed and all warranties expressed or implied are hereby excluded.