How much money do you need to retire? What rate of return on your investments do you need to achieve your “nest egg”?

There are several key tasks you need to complete before you can determine what rate of return you’ll need in order to fund your retirement. These include the following:

- Decide the age at which you want to retire.

- Decide the annual income you’ll need for your retirement years. It may be wise to estimate on the high end for this number. Generally speaking, it’s reasonable to assume you’ll need about 80% of your current annual salary in order to maintain your standard of living.

- Add up the current market value of all your savings and investments.

- Estimate the value of your social security benefits. U.S. residents can obtain their estimated benefits at the Social Security Administration (SSA) website.

A Sample Calculation

Before we begin with our sample calculation, a word on inflation. When drawing up your retirement plan, it’s simplest to express all your numbers in today’s dollars.

Now on to the sample calculation. Consider the hypothetical case of John, a 45-year-old man currently earning $100,000 after taxes. Let’s go through the key factors for John:

- John wants to retire at age 65.

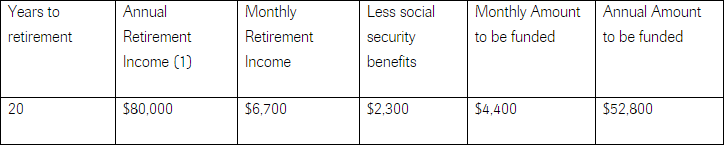

- John will need $80,000 of annual retirement income – in today’s dollars (i.e., not adjusted for inflation).

- John currently has $400,000 in savings and investments.

- Visiting the SSA website, we can quickly calculate John’s estimated social security benefits in today’s dollars. Assuming John is born 45 years ago and will retire 20 years from now, we can retrieve his estimated social security benefits in today’s dollars. The SSA website gives us a value of around $2,300 per month.

1. Based on 80% of his annual earnings.

Now, John determined he would need $80,000 (in today’s dollars) annually to live during his retirement years. To the nearest $100, this works out to about $6,700 per month. Assuming John’s social security funds come through as estimated, we can subtract his estimated monthly benefits from his required monthly income amount.

This leaves him with $4,400 per month that he must fund on his own ($6,700 – $2,300 = $4,400), or $52,800 per year.

John is in good health and has a family history of longevity. He also wants to make sure he can pass along a sizable portion of wealth to his children. As a result, John wants to establish a nest egg large enough to enable him to live off of its investment income – and not eat into his principal amount – during his retirement years.

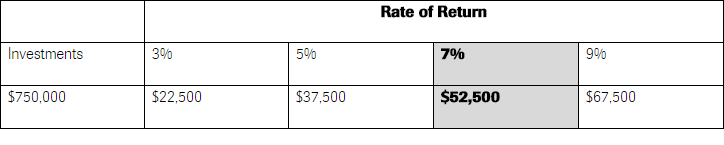

Assuming John will be able to grow his investments to $750,000 (1) by the time he retires he will need a dividend yield of just a fraction above 7% to obtain the $52,800 he will need annually. Seven percent might be possible if dividends increase 3.5%/yr for 20 years. Without any investment appreciation or dividend income, $750,000 would last 14.2 years if drawing out $52,800/year.

This illustrates the importance of monitoring your investment growth rate (3.2%) and the dividend growth rate (3.5%) of your individual holdings or total portfolio. 6.7% total return is not easy to come by today without a great deal of volatility.

Note:

- If John doesn’t invest any more money for the 20 years of retirement, his $400K will grow to $750K by dint of a 3.2% annual return.